Powers of appointment are among the most versatile tools in estate planning. They are often underutilized due to a lack of understanding of their benefits and limitations. At their core, a power of appointment allows an individual, designated by a legal instrument (the “donee” or receiver of the power of appointment), to determine who will receive certain property or interests in the future. The donor, who creates this power, retains flexibility in managing and distributing their estate.

However, caution is necessary when structuring powers of appointment, particularly in the context of the marital deduction. Improperly crafted powers can inadvertently invalidate the marital deduction, leading to significant estate tax consequences. For instance, if a power of appointment does not allow the donee (often the surviving spouse) to appoint property to themselves or their estate, the property may fail to qualify for the marital deduction. This is typically the case with a special (or limited) power of appointment. In contrast, a properly structured general power of appointment can ensure that the property qualifies for the marital deduction, deferring estate taxes until the surviving spouse’s death

Clarification – Donor and Donee Examples

A wealthy individual, the donor of the power of appointment, sets up a trust for their children. The trust includes a special power of appointment allowing the spouse (the donee) to distribute the trust’s assets among their children or grandchildren after the donor’s death. The spouse can decide which child receives what portion of the assets, giving flexibility to address changing family dynamics. This type of power is often chosen to retain control within the family while protecting the assets from the spouse’s creditors and excluding the assets from the spouse’s taxable estate.

A woman (the donor) creates a will that gives her husband (the donee) a general power of appointment over certain assets. This power allows the husband to decide who will inherit those assets upon his death, including the ability to appoint them to himself, his estate, or creditors. This flexibility can be particularly useful in managing taxes and ensuring the estate is distributed according to the most current family needs. However, because the assets are included in the husband’s estate for tax purposes, this power may also increase the taxable estate, potentially leading to higher estate taxes.

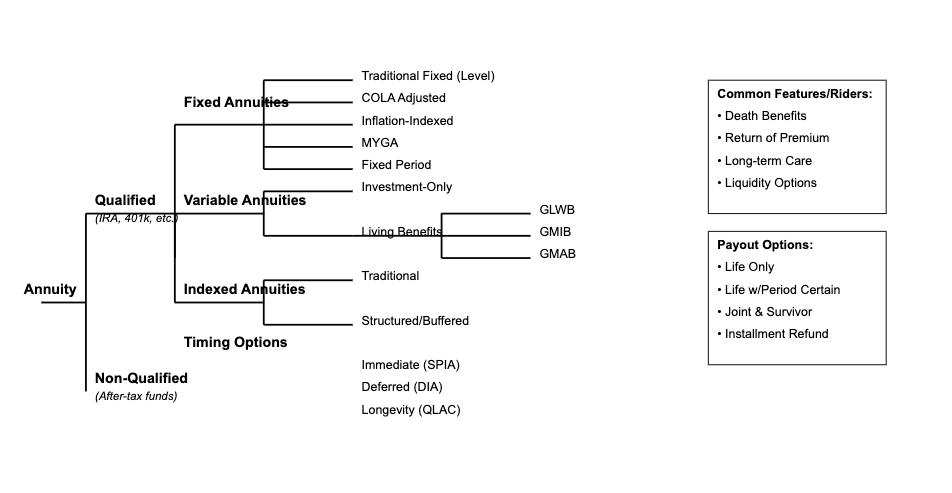

Types of Powers of Appointment

Powers of appointment are classified into several categories:

- Imperative vs. Non-Imperative Powers: Imperative powers must be exercised by the donee, while non-imperative powers are optional.

- Exclusive vs. Non-Exclusive Powers: Exclusive powers allow the donee to exclude certain eligible appointees, while non-exclusive powers require the donee to allocate some property to each appointee.

- General vs. Nongeneral (Special) Powers: General powers allow the donee to appoint property to themselves, their estate, or their creditors. In contrast, nongeneral powers restrict the donee from appointing property to these entities.

- Presently Exercisable vs. Postponed Powers: Presently exercisable powers can be used immediately, while postponed powers can only be exercised at a future date, often upon the donee’s death.

When to use General vs. Limited Powers of Appointment

General Power of Appointment: Best used in Marital Trusts (QTIP) or Revocable Trusts when flexibility, step-up in basis, and marital deduction eligibility are the primary goals, even though the assets will be included in the donee’s taxable estate.

Limited (Special) Power of Appointment: Best used in Irrevocable Trusts, Dynasty Trusts, Bypass Trusts, and Generation-Skipping Trusts where asset protection, tax minimization, control over distribution, and maintaining favorable tax treatment are the main objectives.

| Estate Planning Goal/Consideration |

General Power of Appointment |

Limited (Special) Power of Appointment |

| Asset Protection |

Not recommended. Assets are exposed to the donee’s creditors. |

Recommended. Assets are protected from the donee’s creditors. |

| Typical Trusts |

Rarely used in asset protection trusts. |

Common in Irrevocable Trusts, Dynasty Trusts, and Spendthrift Trusts. |

| Inclusion in Donee’s Taxable Estate |

Recommended when a step-up in basis is desired. |

Not recommended. Assets are generally excluded from the donee’s taxable estate. |

| Typical Trusts |

Marital Trusts (QTIP) for step-up in basis. |

Irrevocable Life Insurance Trusts (ILITs), Generation-Skipping Trusts. |

| Eligibility for Marital Deduction |

Recommended. Ensures property qualifies for the marital deduction, deferring estate taxes. |

Not recommended. May disqualify property from the marital deduction. |

| Typical Trusts |

QTIP Trusts, Marital Trusts. |

Not typically used in marital deduction trusts. |

| Control over Ultimate Distribution |

Provides flexibility but less control over final asset distribution. |

Recommended. Allows the donor to set clear boundaries on asset distribution. |

| Typical Trusts |

Marital Trusts, Family Trusts. |

Family Trusts, Bypass Trusts, Generation-Skipping Trusts. |

| Minimizing Estate Taxes for Donee |

Not recommended. Assets are included in the donee’s taxable estate. |

Recommended. Helps reduce the size of the donee’s taxable estate. |

| Typical Trusts |

Marital Trusts (when step-up is more beneficial). |

Bypass Trusts, Generation-Skipping Trusts. |

| Avoiding Generation-Skipping Transfer Tax (GSTT) |

Not recommended. May trigger GSTT if assets are transferred to skip generations. |

Recommended. Allows for strategic distribution to avoid GSTT. |

| Typical Trusts |

Marital Trusts (with no intent to skip generations). |

Generation-Skipping Trusts, Dynasty Trusts. |

| Flexibility for Changing Family Needs |

Recommended if flexibility to appoint to any individual or entity is desired. |

Provides some flexibility within the confines set by the donor. |

| Typical Trusts |

Revocable Trusts, Marital Trusts. |

Irrevocable Trusts, Family Trusts. |

| Retaining Favorable Tax Treatment in Trusts |

Not recommended. Could disrupt the trust’s tax status. |

Recommended. Helps maintain the trust’s favorable tax status, particularly for pre-existing trusts. |

| Typical Trusts |

Rarely used in older trusts with favorable status. |

Grandfathered Trusts, Irrevocable Trusts. |

| When to Use in Marital Trusts (QTIP) |

Recommended if the intent is to qualify for the marital deduction. |

Not recommended for QTIP trusts as it may disqualify the trust. |

| Typical Trusts |

QTIP Trusts, Marital Trusts. |

Bypass Trusts, Family Trusts (outside of QTIP). |

Table 1. General Overview of the suse of General and Limited(Special) Powers of Appointment in differnt estate plang contexts.

Exercising Powers of Appointment

The exercise of powers of appointment involves several considerations:

- Class of Appointees: The group eligible to receive the property, which can range from specific individuals to broad categories like “descendants.”

- Manner and Methods of Exercise: Powers can be exercised through various methods, including specific or blanket clauses. The intention to exercise must be clear and comply with any conditions set by the donor.

- Capacity to Exercise: The donee must have the legal capacity to exercise the power, similar to the capacity required for property disposition.

Tax Implications

The tax consequences of powers of appointment are significant and complex. Please refer also to Table 1.

- Estate and Gift Tax: A general power of appointment can result in the inclusion of property in the donee’s estate, subjecting it to estate tax. The exercise or release of a general power is treated as a gift for tax purposes.

- Generation-Skipping Transfer (GST) Tax: Exercising a power of appointment can trigger GST tax if it involves skipping generations, though careful planning can mitigate this.

- Income Tax: Under Section 678 of the Internal Revenue Code, the exercise of a general power can result in the donee being treated as the owner of the trust for income tax purposes.

Planning Opportunities

Powers of appointment offer various strategic benefits in estate planning:

- Flexibility: They allow the donee to adapt the distribution of property based on changing circumstances, providing tailored solutions for beneficiaries.

- Extending Trust Terms: Powers can be used to extend the duration of a trust, potentially postponing tax consequences and providing long-term asset protection.

- Generation Jumping: Powers can be used to skip generations, reducing the impact of GST tax by directly benefiting more remote descendants.

Selected Case Law and IRS Private Letter Rulings

The following cases and Private Letter Rulings (PLRs) illustrate the application and interpretation of powers of appointment, particularly general powers of appointment, in the context of federal estate tax law. Specifically, the cases address the tax implications of these powers concerning the marital deduction under Section 2056 of the Internal Revenue Code and whether certain powers of appointment qualify as general powers under Section 2041. Additionally, the cases and rulings explore the implications of trust reformation, particularly how state court modifications of trust instruments may or may not be recognized for federal tax purposes and how these reforms affect the classification and taxability of powers of appointment.

Estate of Kraus v. C.I.R, 875 F.2d 597 (7th Cir. 1989)

Issue

The primary issue in Estate of Kraus v. Commissioner is whether the reformation of a trust by a lower Illinois state court, which corrected a scrivener’s error that omitted a general power of appointment necessary for the marital deduction under Section 2056 of the Internal Revenue Code, should be recognized by the federal Tax Court for estate tax purposes.

Rule

Federal courts, including the Tax Court, are not bound by decisions of lower state courts when interpreting state law for federal tax purposes. According to the precedent established in Commissioner v. Estate of Bosch, only a state’s highest court can issue rulings on state law that are binding on federal courts. Federal courts are required to give “proper regard” to lower state court rulings but are not obligated to follow them if they conflict with federal tax law principles.

Application

In this case, Arthur S. Kraus amended his insurance trust in 1977, inadvertently converting a general power of appointment into a special power due to a scrivener’s error. This error prevented the estate from qualifying for the marital deduction under Section 2056 of the Internal Revenue Code. After Kraus’s death, the estate sought reformation of the trust in an Illinois state court, which granted the reformation, restoring the general power of appointment.

The estate argued that the reformed trust should be recognized by the Tax Court to allow the marital deduction. However, the Tax Court ruled that the state court’s reformation was not binding for federal tax purposes and determined that the trust, as amended in 1977, did not qualify for the marital deduction. The Tax Court found that the estate had not provided sufficient evidence to prove that the omission of the general power of appointment was a mistake warranting reformation under Illinois law.

Furthermore, the Tax Court noted that the decedent, Arthur S. Kraus, was aware of the language necessary to include a general power of appointment, and the amended trust explicitly created a special power instead. This finding was based on the court’s review of stipulated facts, the testimony of attorney Rotman (who drafted the trust amendment), and the original and amended trust documents.

The estate later discovered new evidence that corroborated the claim of a scrivener’s error. The Tax Court initially denied the estate’s motion for reconsideration based on this newly discovered evidence. However, on appeal, the Seventh Circuit Court of Appeals found that the newly discovered evidence was material and likely to change the outcome of the case. The appellate court ruled that the Tax Court abused its discretion in denying the motion for reconsideration and remanded the case for further proceedings.

Conclusion

The Seventh Circuit Court of Appeals affirmed the Tax Court’s decision to uphold the deficiency assessment, agreeing that the original reformation by the state court was not binding for federal tax purposes. However, the appellate court reversed the Tax Court’s denial of the motion for reconsideration, holding that the newly discovered evidence should be admitted and that the case should be reconsidered in light of this evidence. The case was remanded to the Tax Court for further proceedings.

This case illustrates the principle that federal tax courts are not bound by lower state court decisions regarding the reformation of legal instruments when determining federal tax liabilities. It emphasizes the importance of a state’s highest court in issuing binding interpretations of state law for federal purposes.

LTR 9303022 IRS Private Letter Ruling

Issue:

In this case, the issue is whether the reformation of a will by a state court, which retroactively removes a general power of appointment granted to certain beneficiaries, should be treated as a release of that power under Sections 2041 and 2514 of the Internal Revenue Code, thereby subjecting the property to estate and gift taxes.

Rule:

According to Sections 2041(a)(2) and 2514(b) of the Internal Revenue Code, the exercise or release of a general power of appointment is considered a transfer of property and may result in the inclusion of that property in the gross estate of the individual holding the power. See, however, above. Per Estate of Bosch v. United States, the Internal Revenue Service (IRS) is not bound by decisions of lower state courts unless those decisions are consistent with the rulings of the state’s highest court.

Application:

In this case, the Husband and Wife created testamentary trusts that inadvertently granted their Son and Daughter 1 general powers of appointment over their respective trusts, allowing them to invade the trust principal for purposes not limited by an ascertainable standard. This mistake occurred due to an oversight by the law firm drafting the wills, as it failed to include a provision that would restrict the exercise of discretionary powers by beneficiaries who are also trustees.

After the Wife’s death, the Husband petitioned the probate court to reform the trusts to retroactively limit the exercise of the discretionary powers to an independent trustee, thereby preventing the Son and Daughter 1 from holding general powers of appointment. The probate court issued a conditional order to this effect.

The IRS examined whether this reformation constituted a “release” of a general power of appointment, which would trigger estate and gift tax consequences under Sections 2041 and 2514. The IRS concluded that the reformation did not constitute a release because the intent of the Husband and Wife was clearly to prevent their children from holding such powers. The IRS reasoned that, in a bona fide adversarial proceeding, the highest state court would likely deny the Son and Daughter 1 the general powers of appointment before they could become exercisable.

Therefore, the reformation by the lower court would not be considered a release of a general power of appointment under Section 2514, and the trust property would not be included in the taxable estates of the Son or Daughter 1 under Section 2041. Additionally, the reformation did not alter the trust’s status as irrevocable before September 25, 1985, for the generation-skipping transfer tax purposes.

Conclusion:

The IRS ruled that the reformation of the will to limit the discretionary powers of the Son and Daughter 1 did not constitute a release of a general power of appointment. Consequently, the reformation would not cause the inclusion of the trust property in the taxable estates of the Son or Daughter 1, nor would it impact the treatment of the trusts for generation-skipping transfer tax purposes. This ruling was based on the specific facts and applicable law at the time of the request and would not be retroactively applied if there were material fact or law changes.

LTR 9516051 IRS Private Letter Ruling

Issue:

Does the power held by the trustee of a testamentary trust, which allows the trustee to distribute principal to herself as a beneficiary, constitute a general power of appointment under Section 2041 of the Internal Revenue Code?

Rule:

Under Section 2041(a)(2) of the Internal Revenue Code, the value of any property over which the decedent has a general power of appointment is included in the gross estate for estate tax purposes. A general power of appointment is defined under Section 2041(b)(1) as a power exercisable in favor of the decedent, the decedent’s estate, creditors, or the creditors of the decedent’s estate. However, if the power is limited by an ascertainable standard relating to the health, education, support, or maintenance of the decedent, it is not considered a general power of appointment.

Application:

In this case, the decedent was the trustee of a trust created by her deceased spouse’s will, with the power to distribute principal to herself as the beneficiary if, in her sole discretion, it was deemed “requisite or desirable.” This power would generally constitute a general power of appointment under Section 2041, as it allows the trustee to distribute principal to herself without restriction.

However, North Carolina General Statute 32-34(b) imposes limitations on a fiduciary’s power to exercise such discretion. Specifically, the statute prohibits a trustee from exercising a power in favor of themselves, their estate, their creditors, or the creditors of their estate unless the trust document explicitly overrides this limitation. Since the trust document in this case did not override the statute, the decedent, as trustee, did not have a general power of appointment under North Carolina law.

The IRS recognizes that state law governs the creation of legal rights and interests in property, including the scope of powers of appointment. Consequently, under North Carolina law and similar IRS precedents (Rev. Rul. 76-502 and Rev. Proc. 94-44), the decedent’s power as trustee did not qualify as a general power of appointment for federal estate tax purposes.

Conclusion:

The power held by the decedent as trustee of her spouse’s testamentary trust does not constitute a general power of appointment for purposes of Section 2041. Therefore, the value of the trust property is not included in the decedent’s gross estate for estate tax purposes under Section 2041.

Leahy Guiney v. United States of America 425 F.2d 145

Issue:

Does the language in Item Second of Arthur Hamilton Leahy’s will grant his widow a “general power of appointment” sufficient to qualify for the marital deduction under Section 2056(b)(5) of the Internal Revenue Code?

Rule:

Under Section 2056(b)(5) of the Internal Revenue Code, a marital deduction is allowed if the surviving spouse is entitled for life to all the income from the entire interest in the property and has a general power of appointment over the property. A general power of appointment is defined under Section 2041(b)(1) as a power exercisable in favor of the decedent, the decedent’s estate, creditors, or the creditors of the decedent’s estate. The interpretation of whether a power qualifies as a general power of appointment is determined according to the applicable state law.

Application:

In this case, Arthur Hamilton Leahy’s will included language that explicitly stated his intention to grant his widow a “general power of appointment” over the trust assets to ensure that one-half of his estate qualified for the marital deduction. The key issue was whether this language effectively granted the widow the power to appoint the trust principal to herself or her estate, as required by Section 2056(b)(5) of the Internal Revenue Code.

The IRS Commissioner initially denied the marital deduction, arguing that under Maryland law, the language used in the will did not grant the widow a general power of appointment that would allow her to appoint the trust principal to herself or her estate. The District Court upheld the Commissioner’s decision, relying on prior Maryland case law that had narrowly construed similar language as not granting a general power of appointment.

However, upon appeal, the Fourth Circuit considered more recent developments in Maryland law, particularly the decision in Frank v. Frank and the prior decision in Leser v. Burnet by the same court. The appellate court recognized that Maryland courts had evolved to a more modern interpretation that allowed for a general power of appointment when the testator’s intent to grant such power was clear. The court found that the language in Mr. Leahy’s will, which explicitly referred to the “general power of appointment” and the marital deduction under the Internal Revenue Code, was more precise and explicit than the language in previous cases where the power had been found lacking.

The Fourth Circuit concluded that the language used in Mr. Leahy’s will was sufficient to grant his widow a general power of appointment that met the requirements of Section 2056(b)(5) of the Internal Revenue Code, thereby qualifying the estate for the marital deduction.

Conclusion:

The language in Item Second of Arthur Hamilton Leahy’s will effectively granted his widow a general power of appointment over the trust principal, sufficient to meet the requirements for the marital deduction under Section 2056(b)(5) of the Internal Revenue Code. The Fourth Circuit reversed the District Court’s decision and remanded the case for the entry of judgment in favor of the taxpayer.

Special Issues for Fiduciaries and Creditors

Fiduciaries and creditors have specific considerations when dealing with powers of appointment:

- Creditor Rights: Generally, property subject to a nongeneral power is protected from the donee’s creditors. However, property under a general power may be vulnerable, depending on the circumstances.

- Fiduciary Responsibilities: Fiduciaries must carefully manage and exercise powers of appointment, balancing the donor’s intentions with the donee’s interests and tax implications.

Powers of Appointment and Decanting

Decanting, the process of transferring assets from one trust to another, can be facilitated through powers of appointment. This allows for the modification of trust terms, potentially reducing tax burdens and enhancing the trust’s effectiveness.

Conclusion

Powers of appointment are powerful and flexible tools in estate planning, offering both opportunities and potential pitfalls. When structured properly, they can achieve various planning goals, such as securing the marital deduction, ensuring flexibility in asset distribution, and protecting assets from creditors. However, the complexity surrounding the different types of powers—general versus limited—requires careful consideration and precise drafting to avoid unintended tax consequences. The discussed cases and rulings highlight the critical importance of understanding how powers of appointment are treated under both federal tax law and state law, particularly in the context of trust reformation. As illustrated, the reformation of trusts by state courts may not always be recognized for federal tax purposes, emphasizing the need for estate planners to carefully navigate these issues to ensure that the donor’s intentions are fulfilled and tax benefits are preserved. In summary, while powers of appointment are versatile tools, their effective use in estate planning necessitates a thorough understanding of their implications, meticulous drafting, and, where necessary, appropriate legal reformations.

Further Reading

Jonathan G. Blattmachr, Kim Kamin & Jeffrey M. Bergman, Estate Planning’s Most Powerful Tool: Powers of Appointment Refreshed, Redefined, and Reexamined, https://perma.cc/AQ6W-PH72.

![The Rise of Annuities – A Riddle Wrapped in a Mystery Inside an Enigma? [Podcast]](https://i0.wp.com/nationallawforum.com/wp-content/uploads/2024/11/Estate-Planning-Wills-Trusts-Magnifying-Glass.jpg?resize=825%2C510&ssl=1)