The Employee Retention Credit (“ERC”) is a popular COVID-19 tax break that was targeted by some unscrupulous and aggressive tax promoters. These promoters flooded the IRS with ERC claims for many taxpayers who did not qualify for the credit. Now, the IRS is showing mercy and allowing taxpayers to withdraw some ERC claims without penalty.

Many taxpayers were very excited about the ERC, which could refund qualified employers up to $5,000 or $7,000 per employee per quarter, depending on the year of the claim. But the requirements are complicated. Some tax promoters seized on this excitement, charged large contingent or up-front fees, and made promises of “risk-free” applications for the credit. Unfortunately, many employers ended up erroneously applying for credits and exposing themselves to penalties, interest, and criminal investigations—in addition to having to repay the credit. For example, the IRS reports repeated instances of taxpayers improperly citing supply chain issues as a basis for an ERC when a business with those issues rarely meets the eligibility criteria.

After months of increased focus, the IRS halted the processing of new ERC claims in September 2023. And now, the IRS has published a process for taxpayers to withdraw their claims without penalty. Some may even qualify for the withdrawal process if they have already received the refund check, as long as they haven’t deposited or cashed the check.

For those who have already received and cashed their refund checks, and believe they did not qualify, the IRS says it will soon provide more information to allow employers to repay their ERC refunds without additional penalties or criminal investigations.

In this article, we consider whether potentially false or misleading claims about modern slavery (i.e., freedom-washing) may be further called out by Australian regulatory bodies.

‘Freedom-washing’ is a term that can be used to describe a false or misleading claim by an organisation about the positive work being done to identify, assess and combat its modern slavery risks.

Even an understatement or nonstatement of an organisation’s modern slavery risks in its supply chains and operations may be considered ‘freedom-washing’ if it has the intent or effect to mislead the reader (for example, if the organisation’s responses appear overall to be more positive than they would otherwise appear in that light).

‘Freedom-washing’ will not necessarily involve an overtly false action. In some circumstances, a claim may not be entirely accurate despite being partly accurate.

An organisation required to report under the Modern Slavery Act 2018 (Cth) (Modern Slavery Act) needs to carefully consider the information it releases about its modern slavery risks and responses and whether it is potentially engaging in ‘freedom-washing.’

Importantly for all current and future reporting organisations, the scrutiny continues to mount around the legislative framework combatting modern slavery (including in terms of reporting, offences and penalties).

This scrutiny is highlighted by the release of the following recent important reports and studies:

The statutory report of the Modern Slavery Act (see here);

The targeted review of Divisions 270 and 271 of the Criminal Code 1995 (Cth) (see here); and

AUSTRALIAN COMPETITION AND CONSUMER COMMISSION (ACCC) / AUSTRALIAN CONSUMER LAW

As previously reported by K&L Gates, the ACCC has released long-anticipated guidance on environmental and sustainability claims (Guidance—see here), which sets out eight principles that businesses should follow when making environmental and sustainability claims and to comply with the Australian Consumer Law (ACL).

Although the Guidance was issued in the context of making environmental and sustainability claims, in our view, its eight principles can be applied equally to guide businesses in making ‘modern slavery’ claims without breaching the ACL. The Guidance encourages businesses to:

Make accurate and truthful claims.

Have evidence to back up claims.

Not leave out or hide important information.

Explain any conditions or qualifications on claims.

Avoid broad and unqualified claims.

Use clear and easy to understand language.

Remember visual elements should not give a wrong impression.

Be direct and open.

The ACL contains a broad prohibition against businesses engaging in misleading or deceptive conduct and prohibits the making of false or misleading representations about specific aspects of goods or services. As a result, claims that overstate an organisation’s modern slavery commitments generally, or inaccurately portray the working conditions within certain supply chains, may contravene the ACL.

We therefore recommend that organisations should also reflect on the Guidance when preparing a modern slavery statement or releasing information on modern slavery practices.

Breaches of the ACL incur very significant penalties. For corporations, the maximum pecuniary penalty per breach is the greater of:

AU$50 million;

Three times the value of the ‘reasonably attributable’ benefit obtained from the conduct; or

If this benefit cannot be determined, 30% of the corporation’s adjusted turnover during the breach turnover period (being a minimum of 12 months).

The ACCC will consider whether the following factors apply when determining whether to take enforcement action for a breach of the ACL:

The conduct is of significant public interest or concern;

The conduct results in substantial harm to consumers and detriment to business competitors;

Large businesses are making claims on a national scale;

The conduct involves a significant new or emerging market issue, or compliance or enforcement action is likely to have an educative or deterrent effect; or

ACCC action will help clarify aspects of the law, especially newer provisions of the ACL.

Furthermore, the ACCC will take into account the genuine efforts and appropriate steps that were taken by the business to verify the accuracy of any information they relied on.

But is there actually any appetite in the ACCC to seek to enforce the ACL with respect to ‘modern slavery’ claims?

To date, it has not given any indication that ‘modern slavery’ claims will be an enforcement priority. However, the ACCC has demonstrated a willingness to crack down on businesses that have sought to take advantage of increasingly environmentally and socially conscious consumers (e.g. greenwashing). Combined with growing scrutiny and broadening calls for tougher responses to be taken by government and business in combatting modern slavery, the possibility of ACCC action does appear to exist, if not now, then in the not too distant future.

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION (ASIC) / FINANCIAL PRODUCTS AND DISCLOSURE OBLIGATIONS

General Provisions

The Corporations Act 2001 (Cth) (Corporations Act) and the Australian Securities and Investments Commission Act 2001 (Cth) both contain general prohibitions against companies:

Making statements or circulating information that is false or misleading; or

Engaging in dishonest, misleading or deceptive conduct in relation to a financial product or financial service.1

ASIC released Report 763 earlier in the year (read it here), which expanded on its approach to ‘greenwashing’ outlined in Information Sheet 271 (read it here). It detailed ASIC’s recent interventions in response to growing claims from companies, managed funds and superannuation funds about their ESG credentials.

ASIC has expanded both its surveillance and enforcement activities in regards to ‘greenwashing.’ ASIC has pursued civil penalty proceedings and issued infringement notices to companies that are making statements that are false or misleading about ESG ‘greenwashing’ claims.

In light of these actions in the ESG space, we recommend companies be vigilant about the information they include in their modern slavery statements and be careful about the modern slavery disclosures they make in relation to a financial product or service.

Product Disclosure Statements

Under section 1013D(1)(l) of the Corporations Act, if a financial product has an investment component, its issuer must include in the product disclosure statement the extent to which labour standards or environmental, social or ethical considerations are taken into account in selecting, retaining or realising an investment. This is relevant in the modern slavery context where companies are releasing product disclosure statements that refer to modern slavery ESG considerations or make reference to previous market disclosures on modern slavery practices.

ASIC has undertaken reactive and proactive surveillance of product disclosure statements, advertisements, website and other market disclosures. ASIC is also progressing surveillance of the superannuation fund sector on ESG claims.

International Sustainability Standards Board (ISSB) Standards for Disclosure

In addition to ASIC’s enforcement powers, the ISSB has introduced two new standards, IFRS S1 and S2. The standards are likely to be substantially aligned to the mandatory climate-related disclosures in Australia being prepared by the Australian Accounting Standards Board and the Treasury.

Relevant to modern slavery, the new standard IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information requires an entity to disclose information about its sustainability-related risks and opportunities in its general purpose financial reports (read it here).

To achieve the required fair presentation of sustainability-related financial information, an entity is required to provide a complete, neutral and accurate depiction of those sustainability-related risks and opportunities. Additionally, any material information must be disclosed. Information can be material where it omits, misstates or obscures information that could reasonably be expected to influence the decision making of readers of such reports.

‘Sustainability-related risks and opportunities’ are broadly defined as risks and opportunities that could reasonably be expected to affect an entity’s cash flows or access to finance. Anything that impacts an entity’s value chain will be an opportunity or risk to its cash flows. The entity’s work force is an example of a sustainability-related risk and opportunity. Therefore, reporting entities may have to report modern slavery in their supply chains as a material risk to their value chain, particularly if they are operating in a sector where the risk of modern slavery is heightened (for example, renewable energy projects or garment manufacturing).

While compliance with the ISSB standards remains voluntary until codified under Australian law, it is expected that the standards will be widely adopted by companies internationally.

OTHER CONSEQUENCES OF FREEDOM-WASHING

There are many other potential legal consequences of freedom-washing. These include:

Criminal liability under section 137.1 of the Criminal Code Act 1995 (Cth): This offence applies where a person knowingly gives information that is false or misleading or omits any matter or thing without which the information is misleading, and the information is given to a Commonwealth entity;

Breach of directors duties: If directors are not appropriately managing and disclosing the company’s modern slavery risks, then they could be in breach of the duty to exercise skill, care and diligence;

Requisition resolutions: Shareholders may requisition a resolution at the company’s annual general meeting in regards to modern slavery and the company’s supply chain practices; and

Shareholder class action: Shareholders may start a class action if the company has breached continuous disclosure laws by not reporting a modern slavery issue correctly or accurately.

INTRODUCTION OF PENALTIES UNDER THE MODERN SLAVERY ACT

The report on the statutory review of the Modern Slavery Act was released on 25 May 2023.

Its recommendations included that the Modern Slavery Act be amended to provide that it is an offence for a reporting entity to:

Fail, without reasonable excuse, to give the minister a modern slavery statement within a reporting period for that entity;

Give the minister a modern slavery statement that knowingly includes materially false information;

Fail to comply with a request given by the minister to the entity to take specified remedial action to comply with the reporting requirements of the Modern Slavery Act; and

Fail to have a due diligence system in place that meets the requirements set out in rules made under section 25 of the Modern Slavery Act.

The Australian Government has signaled it will now consider Professor John McMillan’s review and will consult across government and with stakeholders in formulating its response to the recommendations. Companies operating business in Australia should watch this space carefully.

We acknowledge the contributions to this publication from our graduate Harrison Langsford.

FOOTNOTES

1 See sections 1041E, 1041G and 1041H of the Corporations Act 2001 (Cth), and sections 12DA and 12DB of the Australian Securities and Investments Commission Act 2001 (Cth).

Clearly, a lot has changed since then, and being aware of and understanding the updates to these Guidelines is crucial for companies, influencers, brand ambassadors, and marketing professionals who engage in influencer marketing campaigns. The Guidelines take into account the evolving nature of influencer marketing and provide more specific guidance on how influencers can make clear and conspicuous disclosures to their followers. This summary provides a basic overview of the key changes and important points to consider in the wake of the updated Guidelines.

Background:

Anyone who has access to the internet is aware that social media influencer marketing has been a rapidly growing industry over the past decade, and the FTC recognizes the need for adequate transparency concerning this area of marketing to protect consumers from deceptive advertising practices.

The general aim of the updated Guidelines is to ensure consumers can clearly identify when a social media post, blog post, video, or other similar media is sponsored or contains affiliate links. The updated Guidelines seek to develop or make clear guidance concerning specifically: (1) who is considered an endorser; (2) what is considered an “endorsement”; (3) who can be liable for a deceptive endorsement; (4) what is considered “clear and conspicuous” for purposes of disclosure; (5) practices of consumer reviews; and (6) when and how paid or material connections need to be disclosed.

Key Changes and Considerations:

Clear and Conspicuous Disclosure: Influencers must make disclosures clear and conspicuous. This means disclosures should be easily noticed, not buried within a long caption or hidden among a sea of hashtags. The Guidelines require that disclosure be “unavoidable” when posts are made through electronic mediums. The FTC suggests placing disclosures at the beginning of a post, especially on platforms where the full content can be cut off (i.e., Instagram). In broad terms, a disclosure will be deemed “clear and conspicuous” when “it is difficult to miss (i.e. easily noticeable) and easily understandable by ordinary consumers.”

Updated Definition of “endorsements”: The FTC has broadened its definition of “endorsements” and what it deems to be deceptive endorsement practices to include fake positive or negative reviews, tags on social media platforms, and virtual (AI) influencers.

Use of Hashtags: The Guidelines still hold that commonly used disclosure hashtags such as #ad, #sponsored, and #paidpartnership are acceptable, but those must be displayed in a manner that is easily perceptible by consumers. Influencers should avoid using vague or ambiguous hashtags that may not clearly indicate a paid relationship. Keep in mind, however, whether a specific social media tag counts as an endorsement disclosure is subject to fact-specific review.

In-Platform Tools: Social media platforms increasingly provide built-in tools for influencers to mark their posts as sponsored. However, be aware, the Guidelines emphasize that these tools can be helpful in disclosing partnerships, but they are not always sufficient to ensure that disclosures are clear and conspicuous. Parties using these tools should carefully evaluate whether they are clearly and conspicuously disclosing material connections.

Affiliate Marketing: If an influencer includes affiliate links in their content, they must disclose this relationship. Simply using affiliate links is considered a material connection and requires disclosure. Phrases such as “affiliate link” or “commission earned” can be used to disclose affiliate relationships.

Endorsements and Testimonials: The FTC guidelines apply not only to sponsored content, but also to endorsements and testimonials. Influencers must disclose material connections with endorsing products, whether they received compensation or discounted/free products. Beyond financial relationships as described above, influencers will need to disclose non-financial relationships, such as being friends with a brand’s owners or employees.

Ongoing Relationships: Disclosures should be made in every post or video if a material connection for benefit exists, even in cases of ongoing or long-term partnerships.

Endorsements Directed at Children: The updated Guidelines added a new section specifically addressing advertising which is focused on reaching children. The FTC states that such advertising “may be of special concern because of the character of audience”. While the Guidelines do not offer specific guidance on how to address advertisements intended for children, those who intend to engage in targeting children as the intended audience should pay special attention to the “clear and conspicuous” requirements espoused by the FTC.

Enforcement and Penalties:

The FTC takes non-compliance with these guidelines seriously and can impose significant fines and penalties on brands, marketers, and influencers who fail to make proper disclosures. Significantly, the updated Guidelines make it clear that influencers who fail to make proper disclosures may be personally liable to consumers who are misled by their endorsements. Furthermore, brands and marketers may also be held responsible for ensuring that influencers with whom they have paid relationships adhere to these guidelines.

Conclusion:

Bear in mind, the Guidelines themselves are not the law, but they serve as a vital guide to avoid breaking it. Overall, the updated Guidelines on influencer disclosures emphasize transparency and consumer protection. To stay compliant and maintain consumer trust, it is imperative that all parties involved in influencer marketing familiarize themselves with these Guidelines and ensure that disclosures are clear, conspicuous, and consistently made in every relevant post or video. Furthermore, as this marketing industry continues to develop and evolve, it will be increasingly important to monitor ongoing developments and changes in the FTC guidelines to stay current with best practices.

Harvard Business Review’s recent survey, “Women in Leadership Face Ageism at Every Age,” shines a bright light on the bleak reality of age discrimination against women in the workplace. The survey of 913 women leaders from across the United States in the higher education, faith-based nonprofit, legal, and health care industries found that supervisors and colleagues find women of every age unfit for leadership roles based on their age. Young women leaders are subjected to head pats and pet names and are often mistaken for students, interns, or support staff. Middle aged women leaders are discounted as having too many family responsibilities or being on the runway to menopause. Older women are largely erased from the work environment, facing assumptions that they are on their way out. This stands in stark contrast to older men, whom employers tend to regard as “wells of wisdom.” In short, when it comes to the workplace, age-related bias perpetually stands between women and recognition as leaders.

Title VII of the Civil Rights Act of 1964 (“Title VII”), which prohibits discrimination in employment, identifies certain “protected classes” upon which bases employers may not discriminate: race, color, religion, sex, and national origin. A separate statute, the Age Discrimination in Employment Act (“the ADEA”), outlaws age discrimination in the workplace. Plaintiffs filing a lawsuit challenging employment discrimination typically must articulate a specific statute their employer has violated. In the case of sex-plus-age discrimination—that is, mistreatment based on the intersection of sex and age—neither statute standing alone captures the plaintiff’s experience.[1] This raises the question of how women facing uniquely gendered age bias in the workplace—like that outlined in the Harvard Business Review survey—can state legal claims a court will consider viable.

For the most part, federal courts have been skeptical of such claims.

A recent case, however, brought a new perspective to the question of sex-plus-age discrimination under federal law. On July 21, 2020, the United States Court of Appeals for the Tenth Circuit, the appellate court that covers Colorado, Kansas, New Mexico, Oklahoma, Utah, and Wyoming, addressed the question “whether sex-plus-age claims are cognizable under Title VII.”[2] In Frappied v. Affinity Gaming Black Hawk LLC, nine female plaintiffs brought (among other claims) sex-plus-age claims for disparate impact and disparate treatment under Title VII, alleging they were terminated because Affinity discriminated against women over forty.[3] The older women, who had worked at the Golden Mardi Gras Casino, were laid off after the defendant purchased the casino in 2012. The terminations were largely unexplained. After the lower court dismissed their claims, the plaintiffs appealed.

The Tenth Circuit ruled in the plaintiffs’ favor, affirming the validity of sex-plus-age claims under Title VII alone. The court noted that it had allowed claims based on a combination of race and sex discrimination in Hicks v. Gates Rubber Co.[4]In Hicks, the court considered the combined effect of racial slurs and sexual harassment in a hostile work environment case. In Frappied, however, the court had to decide a novel question—whether an intersectional discrimination claim could be based on a second characteristic that is not protected by Title VII: age. Most courts that have considered such claims have refused to decide whether a plaintiff can challenge discrimination under an intersectional theory that the combination of the two protected characteristics led to the adverse action, or they have decided the plaintiff can prevail under one statute so the court does not have to decide whether the intersectional claim is viable. For instance, both the Second and Sixth Circuits have sidestepped the issue, making dispositive rulings based on other claims in plaintiffs’ complaints.[5]

In Frappied, the Tenth Circuit noted that the Supreme Court had long held that Title VII prohibits “sex-plus” discrimination where the “plus” factor is not protected under the statute.[6] In Phillips v. Martin Marietta Corp.[7]the Supreme Court held that a policy against hiring women with preschool-age children violated Title VII, because men with preschool-age children were not subject to that policy. Even though “people with preschool-age children” is not a protected class, the Supreme Court recognized this to be a form of sex discrimination. The Tenth Circuit used the same reasoning to hold that if sex—which is protected under Title VII—“play[ed] a role in the employment action,” then the termination was impermissible even though the “plus” factor, age, is in another statute.[8] Borrowing from the Supreme Court’s analysis in Bostock,[9] which held that Title VII’s sex discrimination provision prohibits sexual orientation and gender identity discrimination in employment, the Tenth Circuit held that “if a female plaintiff shows that she would not have been terminated if she had been a man—in other words, if she would not have been terminated but for her sex—this showing is sufficient to establish liability under Title VII.[10]

While the outcome in Frappied is a positive development for civil rights in employment, in most jurisdictions there is no clear protection under federal law against sex-plus-age discrimination. The EEOC has long acknowledged the availability of such intersectional claims, but as mentioned, other sex-plus-age claims have made their way through the courts on occasion without success. The Tenth Circuit is the first and only federal appellate court to formally recognize these claims as viable under federal law.

However, there are state laws that prohibit sex and age discrimination in the same provision,[11] so the federal courts’ unwillingness to combine the effects of discrimination prohibited by two separate statutes is not always a concern. Given the Harvard Business Review’s exposure of the dire state of workplace age bias against women, and the Tenth Circuit’s groundbreaking decision in Frappied, more women experiencing workplace age discrimination may want to consider challenging their employers’ decisions. Because of the variations in protections in different jurisdictions, employees should consider seeking legal advice. If you or someone you know has experienced sex-plus-age bias, contact the experienced lawyers at Katz Banks Kumin today.

[1] The legal standards, particularly the causation standards, also differ under the two statutes. Under Title VII, it is sufficient to prove that sex was a “motivating factor” in an employment decision. Under the ADEA, however, age must be the but-for cause, Gross v. FBL Fin. Serv., Inc., 557 U.S. 167 (2009). Many courts have interpreted this but-for causation standard to mean that if any other reason—even sex, which is a protected class under Title VII—played a role in the employment decision, then the age claims fail. The Supreme Court recently clarified that “but-for cause” does not mean “sole cause,” Bostock v. Clayton County, 140 S. Ct. 1731 (2020), but the idea has yet to trickle down through the federal courts—and into ADEA claims.

[2]Frappied v. Affinity Gaming Black Hawk, LLC, 966 F.3d 1038, 1045 (10th Cir. 2020).

[3]Id.

[4] 833 F.2d 1406, 1416-17 (10th Cir. 1987)

[5]Gorzynski v. JetBlue Airways Corp., 596 F.3d 93, 110 (2d Cir. 2010) (“Having determined that Gorzynski has provided sufficient evidence of age discrimination to reach a jury, there is no need for us to create an age-plus-sex claim independent from Gorzynski’s viable ADEA claim.”); Schatzman v. Cty. Of Clermont, Ohio, No. 99-4066, 2000 WL 1562819, at *9 (6th Cir. 2000) (“[W]e decline the invitation to decide the ‘sex plus [age]’ charge partly because it is unnecessary for us to do so.”).

On November 16, 2022, the U.S. Environmental Protection Agency (EPA) published a much-anticipated supplemental notice of proposed rulemaking (SNPRM) to modify and supplement its 2021 proposed rule that would amend the 2018 Toxic Substances Control Act (TSCA) fees rule. 87 Fed. Reg. 68647. EPA states that “[w]ith over five years of experience administering the TSCA amendments of 2016, EPA is publishing this document to ensure that the fees charged accurately reflect the level of effort and resources needed to implement TSCA in the manner envisioned by Congress when it reformed the law.”

What Action Is EPA Taking?

After establishing fees under TSCA Section 26(b), TSCA requires EPA to review and, if necessary, adjust the fees every three years, after consultation with parties potentially subject to fees. The SNPRM describes proposed changes to 40 C.F.R. Part 700, Subpart C as promulgated in the 2018 Fee Rule (83 Fed. Reg. 52694) and explains the methodology by which EPA determined the proposed changes to TSCA fees. The SNPRM adds to and modifies the proposed rulemaking issued on January 11, 2021 (2021 Proposal) (86 Fed. Reg. 1890). EPA proposes to narrow certain proposed exemptions for entities subject to the EPA-initiated risk evaluation fees and proposes exemptions for test rule fee activities; to modify the self-identification and reporting requirements for EPA-initiated risk evaluation and test rule fees; to institute a partial refund of fees for premanufacture notices (PMN) withdrawn at any time after the first ten business days during the assessment period of the chemical; to modify EPA’s proposed methodology for the production volume-based fee allocation for EPA-initiated risk evaluation fees in any scenario where a consortium is not formed; to expand the fee requirements to companies required to submit information for test orders; to modify the fee payment obligations to require payment by processors subject to test orders and enforceable consent agreements (ECA); to extend the timeframe for test order and test rule payments; and to change the fee amounts and the estimate of EPA’s total costs for administering TSCA Sections 4, 5, 6, and 14. More information on the 2018 Fee Rule is available in our September 28, 2018, memorandum, and more information on the 2021 Proposal is available in our December 30, 2020, memorandum.

The SNPRM includes the following summary of proposed changes to TSCA fee amounts:

Fee Category

2018 Fee Rule

Current Fees1

2022 SNPRM

Test order

$9,8002

$11,650

$25,000

Test rule

$29,500

$35,080

$50,000

ECA

$22,800

$27,110

$50,000

PMN and consolidated PMN, significantnew use notice (SNUN), microbial commercial activity notice (MCAN) and consolidated MCAN

Manufacturer-requested risk evaluation on a chemical included in the 2014 TSCA Work Plan

Initial payment of $1.25M, with final invoice to recover 50 percent of actual costs

Two payments of $945,000, with final invoice to recover 50 percent of actual costs

Two payments of $1,497,000, with final invoice to recover 50 percent of actual costs

Manufacturer-requested risk evaluation on a chemical not included in the 2014 TSCA Work Plan

Initial payment of $2.5M, with final invoice to recover 100 percent of actual costs

Two payments of $1.89M, with final invoice to recover 100 percent of actual costs

Two payments of $2,993,000, with final invoice to recover 100 percent of actual costs

1

The current fees reflect an adjustment for inflation required by TSCA. The adjustment went into effect on January 1, 2022.

2

In the 2018 final rule, the fees for TSCA Section 4 test orders and test rules were incorrectly listed as $29,500 for test orders and $9,800 for test rules. The 2021 Proposal proposes to correct this error by changing the fees for TSCA Section 4 test orders to $9,800 and TSCA Section 4 test rules to $29,500.

Why EPA Is Taking the Action

EPA states that the fees collected under TSCA are intended to achieve the goals articulated by Congress by providing a sustainable source of funds for EPA to fulfill its legal obligations under TSCA Sections 4, 5, and 6 and with respect to information management under TSCA Section 14. According to EPA, information management includes collecting, processing, reviewing, and providing access to and protecting from disclosure as appropriate under Section 14 information on chemical substances under TSCA. In 2021, EPA proposed changes to the TSCA fee requirements established in the 2018 Fee Rule based upon TSCA fee implementation experience and proposed to adjust the fee amounts based on changes to program costs and inflation and to address certain issues related to implementation of the fee requirements. According to the SNPRM, EPA consulted and met with stakeholders that were potentially subject to fees, including several meetings with individual stakeholders and a public webinar in February 2021. EPA is hosting a December 6, 2022, webinar to hear from stakeholders on the proposed TSCA fees. This engagement and the previous stakeholder outreach will inform EPA’s final rule.

According to EPA, based on comments received in response to the 2021 Proposal, adjustments to EPA’s cost estimates, and experience implementing the 2018 Fee Rule, EPA is issuing this SNPRM and is requesting comments on the proposed provisions and primary alternative provisions described that would add to or modify the 2021 Proposal. EPA notes that TSCA allows it to collect approximately but not more than 25 percent of its costs for eligible TSCA activities via fees. EPA states that fee revenue has been roughly half of the estimated costs for eligible activities than EPA estimated in the 2018 Fee Rule, however. According to EPA, the shortfall was, in part, due to EPA’s use of cost estimates based on what it had historically spent on implementing TSCA prior to the 2016 amendments, not what it would cost to implement the Frank R. Lautenberg Chemical Safety for the 21st Century Act (Lautenberg Act). In the first four years following the 2016 Lautenberg Act’s enactment, EPA also did not conduct a comprehensive budget analysis designed to estimate the actual costs of implementing the amended law until spring 2021. In the SNPRM, EPA proposes to revise its cost estimate to account adequately for the anticipated costs of meeting its statutory mandates, which are based on the comprehensive analysis conducted in 2021. EPA states that these proposed revisions are designed to ensure fee amounts capture approximately but not more than 25 percent of the costs of administering certain TSCA activities, fees are distributed equitably among fee payers when multiple fee payers are identified by revising the fee allocation methodology for EPA-initiated risk evaluations, and fee payers are identified via a transparent process.

Estimated Incremental Impacts of the SNPRM

EPA evaluated the potential incremental economic impacts of the 2021 Proposal, as modified by this SNPRM for fiscal year (FY) 2023 through FY 2025. The SNPRM briefly summarizes EPA’s “Economic Analysis of the Supplemental Notice of Proposed Rule for Fees for the Administration of the Toxic Substances Control Act,” which will be available in the docket:

Benefits. The principal benefit of the 2021 Proposal, as modified by this SNPRM, is to provide EPA a sustainable source of funding necessary to administer certain provisions of TSCA.

Cost. The annualized fees collected from industry under the proposed cost estimate described in the SNPRM are approximately $45.47 million (at both three percent and seven percent discount rates (EPA notes that the annualized fee collection is independent of the discount rate)), excluding fees collected for manufacturer-requested risk evaluations. EPA calculated total annualized fee collection by multiplying the estimated number of fee-triggering events anticipated each year by the corresponding fees. EPA estimates that total annual fee collection for manufacturer-requested risk evaluations is $3.01 million for chemicals included in the 2014 TSCA Work Plan (based on the assumed potential for two requests over the three-year period) and approximately $2.99 million for chemicals not included in the 2014 TSCA Work Plan (based on the assumed potential for one request over the three-year period). EPA analyzed a three-year period because the statute requires EPA to reevaluate and adjust, as necessary, the fees every three years.

Small entity impact. EPA estimates that 29 percent of Section 5 submissions will be from small businesses that are eligible to pay the Section 5 small business fee because they meet the definition of “small business concern.” EPA estimates that the total annualized fee collection from small businesses submitting notices under Section 5 is $666,810. For Sections 4 and 6, reduced fees paid by eligible small businesses and fees paid by non-small businesses may differ because the fee paid by each entity would be dependent on the number of entities identified per fee-triggering event and production volume of that chemical substance. EPA estimates that average annual fee collection from small businesses for fee-triggering events under Section 4 and Section 6 would be approximately $103,574 and $2,896,351, respectively. For each of the three years covered by the SNPRM, EPA estimates that total fee revenue collected from small businesses will account for about six percent of the approximately $52 million total fee collection, for an annual average total of approximately $3 million.

Environmental justice. Although not directly impacting environmental justice-related concerns, EPA states that the fees will enable it to protect better human health and the environment, including in helping minority, low-income, Tribal, or indigenous populations in the United States that potentially experience disproportionate environmental harms and risks, and supporting the fair treatment and meaningful involvement of all people regardless of race, color, national origin, or income with respect to the development, implementation and enforcement of environmental laws, regulations, and policies involving TSCA. EPA notes that it “identifies and addresses environmental justice concerns by providing for fair treatment and meaningful involvement in the implementation of the TSCA program and addressing unreasonable risks from chemical substances.”

Effects on state, local, and Tribal governments. The SNPRM would not have any significant or unique effects on small governments, or federalism or Tribal implications.

Commentary

Bergeson & Campbell, P.C. (B&C®) has anticipated the public release of the SNPRM for some time and is not surprised by the proposed increases in fees. We recognize, however, that many readers may review these proposed fees and truly feel a sense of “sticker shock,” as Dr. Michal Freedhoff, the current Assistant Administrator of EPA’s Office of Chemical Safety and Pollution Prevention (OCSPP), cautioned regulated entities earlier this year. B&C has not evaluated the underlying budgetary analysis, so assumes that EPA’s estimate of its costs is accurate. Given that assumption and EPA’s authority to recover 25 percent of those costs, B&C focuses on other aspects of the proposal.

Taking an optimistic view, the increase may benefit regulated entities. EPA states in the SNPRM that “Collecting additional resources through TSCA fees will enable EPA to significantly improve on-time performance and quality.” The absence of these two metrics, as well as others, has mired EPA’s activities under TSCA Sections 4, 5, and 6 for years. The influx of funding, along with proper leadership, training, and management, will aid EPA with meeting its statutory deadlines under TSCA, and the transparency elements of its Scientific Integrity Policy and the scientific standards under TSCA Section 26. Below, we provide representative examples of how the fees increase will aid EPA with avoiding the repetitious shortcomings that have permeated its decision making under TSCA Sections 4, 5, and 6.

TSCA Section 4

B&C notes that EPA states the following about its intended use of its order authority under TSCA Section 4: “The Agency believes it is reasonable to assume that approximately 75 test orders per year will be initiated between FY 2023 and FY 2025. Approximately 45 of these test orders are expected to be associated with the Agency’s actions on PFAS.” In comparison, EPA has issued 20 TSCA Section 4 test orders on 11 existing chemical substances since March 2020. The issued test orders have, however, suffered from significant lapses in transparency. as well as outcomes that conflict with the scientific standards under TSCA Section 26 and the obligations under Section 4.

These concerns with transparency and EPA’s failure to meet the scientific standards under TSCA Section 26 are likely due in part to EPA’s resource and staffing limitations. Therefore, the increased cost of test orders from $11,650 to $25,000 will enable EPA to develop test orders that are focused on data needs, rather than data gaps, during its prioritization and risk evaluation activities. It will also provide EPA with the requisite funding to ensure that it responds timely to technical inquiries from test order recipients, rather than months and in some cases more than a year later.

TSCA Section 5

B&C has decades of experience reviewing EPA’s assessments on new chemical substances under TSCA Section 5. Of relevance here are our observations since TSCA was amended in 2016. Since this time, we have observed a decrease in transparency in EPA’s risk assessments on new chemical substances. For example, EPA routinely identifies analogs from which it reads across potential hazards for new chemical substances. It is not uncommon, however, for EPA to identify multiple analogs for doing so. What is common is that EPA selects an analog amongst many and does not state the scientific basis for the selected analog. This also applies to analogs identified by submitters that are often dismissed by EPA without a scientific basis for doing so. Furthermore, EPA routinely claims those analogs as confidential business information (CBI) without reviewing whether they are actually still confidential. It is important for EPA to protect legitimate CBI, but the statute also requires disclosure of information that is not actually CBI. Additional resources will allow EPA to update its databases to reflect the current state of CBI claims and to better evaluate whether old CBI claims are still justified.

We also hope that additional resources will enable EPA to rely on fewer “worst-case” shortcuts in its evaluations of PMNs. For example, EPA routinely uses the acute potential dose rate (PDR) as the exposure metric for assessing potential unreasonable risks, even when the hazard is a chronic effect. Evaluating against a PDR is a reasonable first pass calculation — if EPA does not identify risk using a PDR, no further evaluation is necessary. We do not, however, agree with EPA making unreasonable risk determinations on the screening-level assessments without further refinements — it is simply not justifiable scientifically to predict chronic risk using a PDR (as reflected in EPA’s assessments under Section 6). Performing the refined calculation requires additional effort, which the fee rule would help support.

We expect EPA will resolve the above issues with the increased funding that it intends on receiving for new chemical substance notifications (e.g., from $19,020 to $45,000 on PMNs). EPA states that the “Additional funding collected through TSCA section 5 fees will help EPA reduce the backlog of delayed reviews and support additional work for new cases.” These monies will also provide EPA the necessary budget to better justify the selection of analogs. Collectively, we hope these improvements will allow EPA’s risk assessors to exercise their inherently government function of evaluating and approving and/or modifying the contractor-generated work products as EPA-approved work products. This will provide more transparent and timely evaluations on novel chemistries notified to the Agency. This level of transparency will also ensure that EPA is satisfying its requirements under EPA’s Scientific Integrity Policy, which states “At the EPA, promoting a culture of scientific integrity is closely linked to transparency. The Agency remains committed to transparency in its interactions with all members of the public.” In doing so, EPA will additionally be providing risk assessments that clearly document its decision making and how those decisions satisfy the scientific standards under TSCA Section 26. These considerations are critical for submitters, not in the sense that they must agree with EPA’s determinations, but rather that they understand the bases for those determinations.

Unanswered questions about when the increased fees will improve the throughput of new chemicals reviews remain. Hiring and training staff takes time; EPA is currently working to fill open positions and train new staff. Submitters paying substantially higher fees would reasonably expect that EPA improve its performance or, if EPA cannot complete timely its reviews (absent suspensions by the submitter), expect that EPA would refund the submission fee.

TSCA Section 6

B&C views the fee increases for EPA’s administration of TSCA Section 6 as the most controversial, not necessarily because of the intended increased costs, which are substantial (e.g., EPA-initiated risk evaluation from two payments resulting in $2,560,000 to two payments resulting in $5,081,000), but rather because of EPA’s decision making in the risk evaluations and its incorporation of new policy directions into its revised risk determinations. EPA has stated that its revisions to the final risk evaluations on eight of the “first 10” chemical substances and accompanying revised risk determinations are “supported by science and the law.” EPA spent the last year revisiting its risk determinations, with little change other than EPA’s conclusion about the “whole chemical.” EPA has not addressed weakness in the risk evaluations identified by commenters; nor has EPA addressed the weaknesses in EPA’s systematic review process identified by the U.S. National Academies of Science, Engineering, and Medicine’s (NASEM) review of EPA’s “Application of Systematic Review in TSCA Risk Evaluations.” NASEM’s review concluded that “The OPPT approach to systematic review does not adequately meet the state-of-practice [and] OPPT should reevaluate its approach to systematic review methods, addressing the comments and recommendations in this report.” The foregoing issues are troubling and are expected to be contested by regulated entities when EPA proposes its draft risk management rules on the “first 10” chemical substances. EPA did, however, state in the SNPRM that:

Although section 6 cost estimates were informed by risk management and risk evaluation activities for the first 10 chemicals, EPA will not be recovering fees for those chemicals.

Though this may seem like a hollow victory for potentially regulated entities, given EPA’s risk determinations on these substances, the intended fees for the EPA-initiated risk evaluations at least provide a baseline of deferred costs that may be allocated for disputing scientific and legal shortcomings when EPA issues the draft and final risk management rules. Moving forward, we anticipate that EPA will use the intended increased funding from the various risk evaluation costs to ensure that the above issues are addressed in its future risk evaluations on high-priority substances.

Conclusions

B&C recognizes that its position on the proposed fees increase in the SNPRM may not be well received by regulated entities. We note that the increased fees will aid with decreasing uncertainty in EPA’s decision making and its timely completion of evaluations on new and existing chemical substances and improve transparency and documents that meet the scientific standards under TSCA Section 26. There is also no question that EPA has the statutory authority to raise fees to recover 25 percent of its costs. B&C’s view is that commenters should focus on the distribution of the fees among the categories, proposed exemptions, and other aspects of the rule, including when manufacture or import must cease to avoid paying fees, rather than focusing on the magnitude of the fee increase.

We also hope that regulated entities will welcome EPA’s use of the best available science and weight of scientific evidence in its risk evaluations. As we discussed above, these statutory requirements have not been met in the “first 10” risk evaluations. We recognize that the deadlines for risk evaluations are not necessarily the critical issue for regulated entities, rather it is EPA’s unreasonable risk determinations, which are based on risk evaluations that were developed in a manner inconsistent with TSCA Section 6 and the implementing regulations. The increased fees under TSCA Section 6 should aid with addressing these issues.

Finally, B&C is optimistic that the SNPRM will provide EPA with the requisite funding to ensure its successful oversight of activities under TSCA. Despite our optimism, we do recognize that increased funding alone will not improve EPA’s administration of TSCA. To ensure success, EPA’s leadership will have to manage and lead this program properly. These latter components are critical and if the SNPRM is promulgated as, or as close to as proposed, the expectation on this Administration to produce results will be sky high.

In recognition of National Estate Planning Awareness Week, we sat down with Lindsey Paige Markus, a principal with Chuhak & Tecson law firm in Chicago to discuss the top estate planning challenges and considerations that her clients face. Markus oversees Chuhak & Tecson’s 24-attorney estate planning and asset protection group, and focuses her practice on counseling business owners and families in planning their estates, minimizing taxation and transferring wealth.

Read on to learn more about Markus’ key tips for successful estate planning, and how clients can tailor their estate plans for any stage of their lives.

The NLR: Estate planning needs can change throughout a person’s lifetime. How do you counsel clients to navigate these changes, whether it be marriage, having children or divorce?

Markus: Over time, assets and relationships may change. You might not have the same relationship with the individuals you selected to act as executor or trustee. You may also disagree on how the couple you identified to care for minor children have parented their own children at the last family gathering. Asset holdings, values and priorities change. When your children were young, you may have been very concerned with there being sufficient resources to provide for their everyday needs and help fund a college education. If they are now successful adults living on their own, you might wish to prioritize leaving a philanthropic legacy to your community. Similarly, laws and tax exemptions change over time. For these reasons, I often recommend that clients revisit their estate plan every three years to confirm that the individuals they have identified to carry out their wishes are still appropriate, in addition to the division of assets.

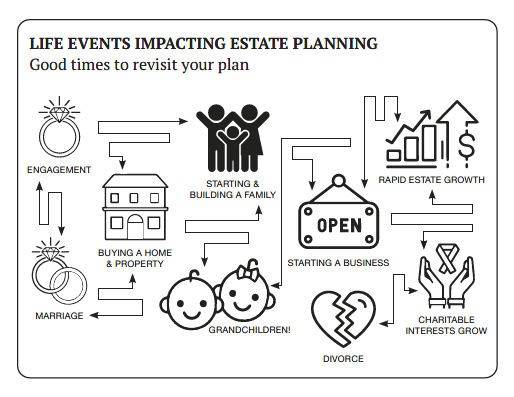

The following image from my book, “A Gift for the Future – Conversations About Estate Planning,” helps highlight life events impacting estate planning, including the following:

– Engagement

– Marriage

– Buying a home or property

– Starting and building a family

– Welcoming grandchildren

– Starting a business

– Rapid estate growth

– Charitable interests grow

– Divorce

The NLR: How can clients prepare to handle probate and guardianship issues?

Markus: Ideally, clients will take the time to get documents in place so that their loved ones can avoid probate and guardianship proceedings. Often a revocable living trust is the most efficient vehicle to ensure that the court system is avoided during one’s life (guardianship proceedings) and upon death (probate). When properly drafted, the trust can also help to leverage estate tax savings, provide asset protection for beneficiaries and ensure that the maximum amount can pass estate-tax free from generation to generation. But it is not enough to simply have an estate plan with a revocable living trust. Rather, clients need to go through the process of funding their trust – retitling assets into the name of the trust, transferring real estate interests, business interests and making certain that beneficiary designations on life insurance and retirement plan assets comport with the overall plan.

The NLR: What do you think are some of the biggest or most common misconceptions people have about estate planning?

Markus: People think that “estate planning is for the rich and famous,” or comment, “I will make an estate plan…when I have an estate to plan!” In reality, everyone should have an estate plan in place to document their wishes and make the process more manageable for their loved ones. Estate tax savings are just one aspect. But anyone who has had the displeasure of going through the probate process appreciates the importance of avoiding it. Too often clients are overwhelmed by the process. In reality, like any project, actually engaging in the planning and getting it done is far easier than procrastinating. And once you find an estate planning attorney that you feel comfortable working with, the attorney should be able to help guide you seamlessly through the process. Clients are often surprised by how empowering the estate planning process can be.

The NLR: Estate taxes owed to federal and state governments can be difficult to deal with for many people. How can clients best navigate challenging estate tax situations?

Markus: Estate tax liabilities at the federal and state levels can easily reach a tax rate of 50%. FIFTY PERCENT! As challenging as it is to consider, those with taxable gross estates can’t afford to avoid planning. In contrast, by engaging in thoughtful estate planning, these estate tax liabilities can be minimized and sometimes completely eliminated. The best advice I have for clients is to engage in planning early. Once you see projections of your future net worth based on your life expectancy, you quickly appreciate the size of the potential tax liability. You will need to provide feedback on your goals of planning. And, from there, your estate planning attorney, working in tandem with your wealth advisor and CPA, can help advise you on proactive steps you can take now to help minimize or avoid those tax liabilities. Maybe it is through implementing an annual gifting program where you use the annual gift exclusion of $17,000 per person per year by making a gift outright or to a trust for the benefit of a loved one. Perhaps you are in a position to use your $12.92 million lifetime exemption before it cuts in half in 2026. The real benefit of gifting is that we can move the current value of the gift and all future appreciation outside of your taxable gross estate. Or, some clients elect to engage in life insurance as an estate tax replacement vehicle – they purchase life insurance to provide the family with liquidity to cover the estate tax in the future.

The NLR: What are some of the most common mistakes you see people make when it comes to estate planning, and how can they avoid them?

Markus: Start early! None of us know what the future has in store. Get your plan in place this year – and make modifications in the future. Fund your trust! Don’t just get an estate plan. Make sure you retitle assets into your trust and update beneficiary designations to leverage the benefits of the plan. Don’t forget about charitable intentions! It is so easy to leave a lasting legacy to a cause you are passionate about. In doing so, follow your estate planning attorney’s advice and consider leaving taxable retirement plan assets directly to the charity. That allows the funds to pass estate-tax free and income-tax free, sometimes saving more than 70% in estate and income tax consequences. Revisit your plan every three years. Review the summary of your plan, make certain your assets were properly moved into your trust and follow-up with your attorney to find out if any changes have taken place in the law which would warrant an update.

Since 2004, New York has provided tax credits to encourage film and television productions located in the state. In its adopted budget for fiscal year 2024, the tax credit program was extended to 2034, and the amount available for the tax credit increased to $700 million. The credit is 30% of “qualified costs” incurred in the production. This tax credit is one of the reasons that New York has remained one of the top filming locations in the United States notwithstanding stiff competition from other states to lure television and film projects.

Subsequently, legislation (S7422A) was introduced that would remove from “qualified costs” used to calculate the tax credit any production that “uses artificial intelligence in a manner which results in the displacement of employees whose salaries are qualified expenses, unless such replacement is permitted by a current collective bargaining agreement in force covering such employees.”

Given that the purpose of the tax credit is to incentivize production and creation of jobs in the state, with the increasing use of artificial intelligence (AI), there is scrutiny of how AI will impact/employment in film and television productions. The legislators were also aware that the use of AI was a major issue in the recent negotiations for contracts with the writers (now settled) and actors (still ongoing as of this date). Consequently, the idea to disincentivize the use of AI that supplants employment by removing the cost of AI from the calculation of the tax credit provides motivation to pursue the proposed legislation in New York’s Legislature.

The goal of removing AI costs from the credit is protecting employment from encroachment by AI, but how the disallowance would be implemented is unclear. For example, if instead of using costumed characters or extensive make-up, a production used computer generated images (CGI), would the cost of the CGI be disallowed? Or if AI were used to write or supplement dialogue, would that call into question those costs for computing the tax credit? How would an auditor reviewing the film credit know and understand where AI is used and whether it actually displaced a human employee? In addition, auditors would have to examine collective bargaining agreements to determine whether “such replacement is permitted by a current collective bargaining agreement in force covering such employees.”

On September 29, 2023, the U.S. Supreme Court granted certiorari in Bissonnette v. LePage Bakeries Park St. LLC, a case from the Second Circuit Court of Appeals involving application of the Federal Arbitration Act’s (“FAA”) exemption for transportation workers.

Specifically, Section 1 of the FAA exempts from arbitration “contracts of employment of seamen, railroad employees, or any other class of workers engaged in foreign or interstate commerce”—the third category commonly referred to as the “transportation worker” exemption.

In the case below, the plaintiffs—a group of delivery drivers for a bakery—filed various wage and hour claims against the defendant, whom they claimed was their employer. When the defendant moved to compel arbitration, the plaintiffs argued that, as bakery delivery drivers, they were exempt from arbitration as a “class of workers engaged in foreign or interstate commerce.”

The Second Circuit concluded that the plaintiffs were not exempt from arbitration because they were in the bakery industry, not in the transportation industry. Therefore, the Second Circuit concluded that the plaintiffs were not transportation workers subject to exemption under Section 1 of the FAA. The Second Circuit’s decision turned, in part, on the interpretation of the U.S. Supreme Court’s decision in Saxon—a case that we previously reported on from last term.

In the Saxon case, the U.S. Supreme Court unanimously held that a ramp supervisor who frequently handled cargo for an interstate airline company was exempt under Section 1 of the FAA as a transportation worker. In reaching that conclusion, the U.S. Supreme Court’s analysis focused on the “actual work” the worker performed, rather than the industry in which the employer operated—holding that “[the worker] is . . . a member of a ‘class of workers’ based on what she does at Southwest, not what Southwest does generally.”

Though the Second Circuit in Bissonnette acknowledged Saxon, the Second Circuit, in a split decision, held that Saxon did not come into play, stating that “those who work in the bakery industry are not transportation workers, even those who drive a truck from which they sell and deliver the breads and cakes”—essentially establishing a threshold requirement that the individual work in the “transportation industry” in order to be covered by the exemption.

In a pointed dissent, Judge Pooler wrote: “Of course these truckers are transportation workers,” and, “[b]y focusing on the nature of the defendants’ business, and not on the nature of the plaintiffs’ work, the majority offers the sort of industrywide approach Saxon proscribes.”

The U.S. Supreme Court’s forthcoming decision will likely clarify whether the FAA’s exemption contains an industry requirement or whether the analysis turns purely on the nature of the work the individual worker performs without regard to the underlying industry in which they work. Regardless of the outcome, the U.S. Supreme Court’s decision will provide much-needed guidance at a time when more and more businesses are bringing transportation services in-house—opting to ship and deliver their own products as opposed to relying exclusively on traditional transportation companies.

The United Stateshas halted immigrant and nonimmigrant visa services in Israel amid ongoing security concerns.

Key Points:

Visa services are unavailable at this time at the U.S Embassy in Jerusalem or the Embassy Branch Office in Tel Aviv. Non-U.S. citizens in need of emergency visa services should request an expedited appointment at a U.S. embassy or consulate other than Jerusalem or Tel Aviv.

U.S. citizens in Israel, the West Bank or Gaza who would like assistance should fill out this crisis intake form, which allows the U.S. State Department to respond to requests from evacuees in leaving or obtaining other routine or emergency passport or citizen services or information.

Commercial flight availability remains limited out of Ben Gurion Airport, but the U.S. government is facilitating charter flights and other modes of transportation for U.S. citizens. The State Department said these flights will continue until at least Oct. 19.

The Israeli government has extended the validity of work visas until Nov. 9, 2023, for all foreign nationals in the country whose Israeli visas will expire within the next month.

BAL Analysis: Visa services are not available in Israel at this time. The situation continues to evolve and travel rules and procedures may change with little or no notice. U.S. citizens in Israel are encouraged to monitor State Department websites for updates.

California recently passed a groundbreaking new law aimed at further regulating the data broker industry. California is already one of only three states (along with Oregon and Vermont) that require data brokers—businesses that collect and sell personal information from consumers with whom the business does not have a direct relationship—to meet certain registration requirements.

Under the new law, the regulation of data brokers—including the registration requirements—falls within the purview of the California Privacy Protection Agency (CPPA) and requires data brokers to comply with expanded disclosure and record keeping requirements. Notably, the law also requires the CPPA to make an “accessible deletion mechanism” available to consumers at no cost by January 1, 2026. The tool is intended to act as a single “delete button,” allowing consumers to request the deletion of all of their personal information held by registered data brokers within the state.

Putting it into practice: Businesses considered “data brokers” should carefully review the new and expanded requirements and develop a compliance plan, as certain aspects of the law (e.g., the enhanced registry requirements) go into effect as soon as January 31, 2024.